Market Commentary - Summer 2025

Read the Summer 2025 WAA for our Market QuickTakes, Q2 Review, and Much More

July 2025

Second Quarter Market Recap: Volatility, Recovery & Resilience

The second quarter of 2025 was one of the most volatile periods in market history, marked by extreme swings in sentiment driven by tariff policy shocks, inflation concerns, and economic uncertainty. It tested the resolve of even the most seasoned investors—requiring discipline, patience, and long-term perspective to weather the storm.

Markets were rattled in early April following President Trump’s surprise "Liberation Day" tariff announcement on April 2, triggering a sharp downturn. However, this was quickly reversed by an unprecedented 90-day reciprocal tariff pause on April 9, following an overnight revolt in the bond market. The market surged in response, with that single day accounting for over 80% of April’s recovery gains.

Recession risks surged to 50–60%, while inflation expectations spiked to post-2022 highs—both calming somewhat after the tariff pause. The Fed, though holding rates steady, acknowledged elevated uncertainty, slowing growth, and rising price pressures.

Momentum from the April 9 rally carried through May and June, propelling the S&P 500 and Nasdaq to new all-time highs by quarter-end. The tech-heavy Nasdaq, after a sharp 23.9% drawdown, closed Q2 up 5.5%, while the S&P 500, down 18.9% at its low, also finished the quarter up 10.6%—both ending the First Half at record levels.

Strong Returns for Diversified Investors

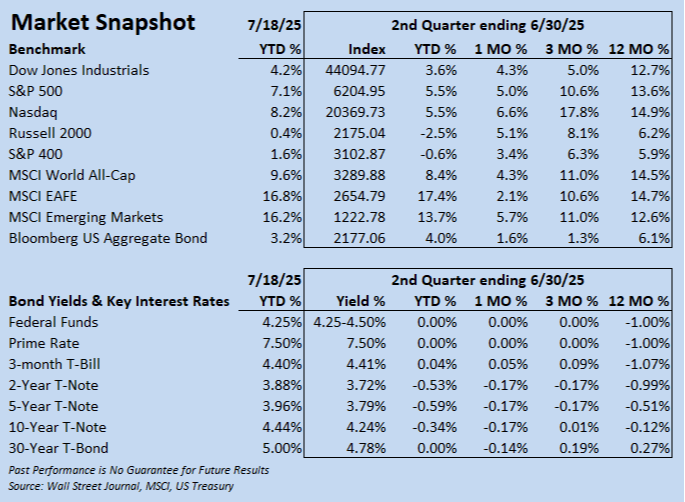

Despite volatility, Q2 delivered robust returns, with Nasdaq leading the charge, gaining 7.8% in Q2 and closed the First Half +5.5% YTD and at all-time highs. The benchmark S&P 500 finished +10.6% in Q2 and also closed the First Half +5.5% YTD and at all-time highs. The Dow Jones Industrials gained 5% in Q2 and finished in positive territory YTD +3.6%. Small- and mid-cap stocks made strong recoveries from April 2, gaining 8.1% and 6.3% in Q2 but finished the First Half in negative territory. Whether measured by the Dow, S&P 500, or Nasdaq, the market recovery has been one of the fastest on record in modern history.

Q2 corporate earnings growth is now expected to slow to 5% from 9.4% at the start of the quarter, according to FactSet, further stretching stock valuations at current levels. Jobs data remained solid, with unemployment steady at 4.2% in May. Inflation reports (CPI and PPI) came in better than expected, supporting the market's bullish rebound as recession risks eased, though remain elevated.

Overseas, the impact of the April 2 "Liberation Day" tariff announcement was global, also hitting foreign markets but much less severely than in the US, with modest currency impact. The benchmark MSCI EAFE index continued to outperform US counterparts even at the tariff low and strongly participated in the post tariff pause recovery as well; the MSCI EAFE index gained 10.9% in Q2, set all-time highs along the way and closed the first half up 17.4% in US dollar terms. Meanwhile, the MSCI Emerging Markets gained 11% in Q2, recovering from its 13.4% max tariff decline to finish the first half up 13.7%; the US dollar fell 10.7% in the First Half.

Timing the Market: A Risky Game

Missing just one key day—April 9—meant missing a massive portion of the recovery. That single session delivered 8–12% gains across major indexes. By the end of April, it represented over 80% of the recovery gains. By quarter-end, up to one-third of total recovery gains had still come from that day alone.

Interest Rates Volatile, But Anchored

As expected, the Fed kept policy interest rates unchanged in the Second Quarter at both FOMC meetings, and maintained its 2025 rate-cut projection at two, citing continued uncertainty around tariff policy, raised inflation expectations, and slowing economic growth (though recession risks have moderated), while headline inflation measures remained muted in delay of tariff impact.

The 10-year Treasury yield closed Q2 at 4.24%, nearly flat, despite hitting a high of 4.59%. Long-term rates rose more meaningfully—30-year Treasury yields climbed 19 bps to 4.78%, reflecting debt concerns tied to proposed fiscal policy.

Geopolitical and Fiscal Pressures Rising

The Israel-Iran conflict added to market jitters, particularly in energy prices. Meanwhile, the prospect of the “One Big Beautiful Bill” (OBBB) raised fresh fiscal questions, with projections suggesting it may add $3–$5 trillion to the national debt over a decade (JPMorgan).

July Market Update: New Highs and Cautious Optimism

July has seen continued momentum, with the S&P 500 and Nasdaq posting additional gains of 2.6% and 3.0%, respectively ending July 18, setting multiple all-time highs. The Dow Jones Industrials, small-cap Russell 2000, and mid-cap S&P 400 have extended their gains as well, with the latter benchmarks moving back into positive territory YTD.

Developed international markets have moderated slightly in July after strong First Half performance, though the MSCI EAFE index has also posted new highs. Emerging Markets continue to show strength amid a weaker dollar and have extended First Half gains.

President Trump’s OBBB Act was signed into law on July 4. While expanding tax cuts and fiscal stimulus, the projected long-term debt impact has unnerved bond markets, pressuring yields higher, especially on the long end of the curve. The Fed meets again July 29-30 and is expected to leave interest rates unchanged, despite President Trump’s pressure to cut rates and persistent talk of replacing Chair Powell before his term ends in May 2026, which has unnerved the bond market.

The Outlook: Volatility Remains a Theme

While the market’s resilience and speed of recovery have been encouraging, uncertainty remains elevated. Tariff policy, inflation dynamics, and geopolitical instability all suggest the potential for continued turbulence. Investors are reminded that:

Missing even one key day can have long-term consequences. Staying invested, diversified, and disciplined is essential in volatile markets.

We continue to monitor developments closely and urge a balanced approach—remaining invested while prepared for near-term choppiness.

It is important investors:

- Remain well-diversified

- Maintain discipline and patience

- Focus on the long-term

- Review your Risk Tolerance

Call your Nelson Advisor today at 800-345-7593 to discuss any concerns and review your portfolio.

~Your Nelson Securities Team

*Past Performance is No Guarantee for Future Results; This article is for informational purposes only and does not constitute investment advice.