Market Commentary - January 2024

Read the Winter 2024 WAA for our Market Quicktakes, Q4|2023 Review and 2024 Outlook, and Much More

January 2024

Stocks and bonds surge in November and December

to cap very strong 2023 overall

2023 was a remarkable year for the global financial markets, posting strong gains across the board for both stocks and bonds. But it took investor resolve and discipline to reap the rewards, providing yet another example of the perils of trying to time the market.

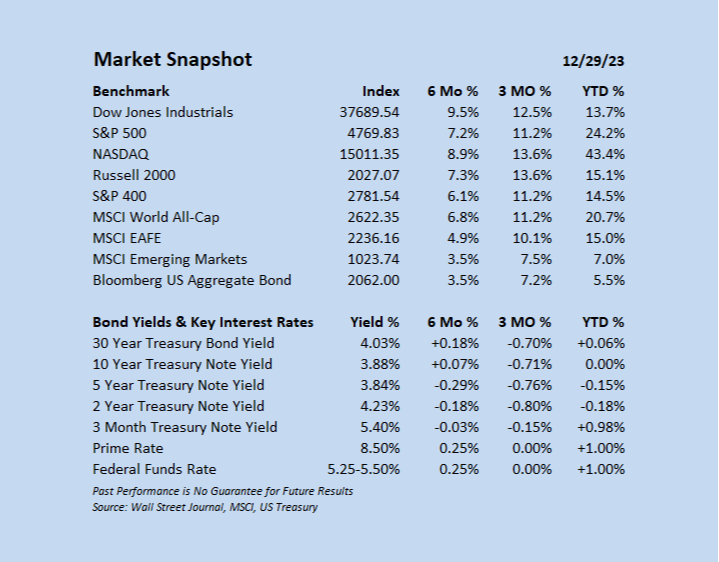

Mega-cap technology and large-cap growth stocks dominated the US markets in 2023, with the Nasdaq Composite gaining 43.4% and leading the charge. More specifically, the Magnificent Seven dominated: Apple, Alphabet (Google), Amazon, Nvidia, Microsoft, Meta (Facebook), and Tesla. For the year, these concentrated tech mega-caps gained over 100% on average and generated more than 60% of the S&P 500’s gains for the year. The benchmark S&P 500 surged 24.2% and closed within about half a percent of an all-time high. The Dow hit an all-time high in December and closed up 13.7% for the year ending at 37,690. Small- and mid-cap stocks led the market over November and December, showing encouraging market breadth, to finish up 15.1% and 14.5%, respectively. US stocks posted double-digit gains over November and December to cap the impressive 2023 gains overall, which were largely a reversal of 2022 performance.

Overseas, developed markets, as measured by the MSCI EAFE index, jumped 15% thanks to a November and December double-digit surge as well. Emerging market returns were more subdued for the year gaining 7% in 2023, as China largely dragged on performance.

In 2022, most economists and market strategists predicted a major recession to hit the US economy in 2023, which led to an extremely volatile. The Fed started raising interest rates in March 2022 to slow the economy, battle inflation, and reverse emergency policy. Covid enhanced inflation, largely from supply chain constraints, energy, and rents, still hit 1980s levels by June peaking at 9.1%. Interest rates spiked, amid seven Fed rate hikes and guidance for more, disrupting the global markets with double-digit losses for both stocks and bonds in 2022, unnerving investors.

The recession forecast prevailed for the beginning of 2023 but gradually shifted to a soft-landing/mild recession outlook through the year. The widely forecasted recession never showed up and the US economy broadly outperformed expectations and the markets responded positively. Supply chains were mostly restored to normal and energy costs fell sharply. Not only did GDP continue to hit all-time highs in 2023, but the US economy also grew over 4.9% annualized in Q3 and an estimated +2.2% in Q4. Unemployment hit 50-year lows, closed 2023 at 3.7% and has remained below 4% for over 22 months ending the year. It’s remarkable that in April 2020 and amid the throws of the Covid-19 pandemic, unemployment hit 14.8%. We have come a long way.

The road for the market in 2023 had some large bumps along the way, including a spring pullback and a Fall correction. Debt ceiling shenanigans in Congress resulting in a downgrade in US credit ratings, and Fed guidance that higher-for-longer interest rate policy would prevail, threw the market a curveball to start August and ended a 5-month winning streak. Interest rates reversed and spiked higher, disrupting the stock and bond markets from August through most of October. Overall, 2023 was significantly less volatile than 2022. There were 122 days of +/- 1% for the S&P 500 in 2022, while in 2023 there were just 64, which is about the long-term average (Goldman Sachs). The most common volatility measure (VIX) settled the year at 12.45, down 43% from 21.67 at the end of 2022, and well-below its long-term average of 20.

Interest rates were front and center all year for the global financial markets. Coming off the worst year in history for the bond market, as interest rates rose sharply across the yield curve in 2022 and the Fed raising policy rates seven times, bonds were poised for a rebound. While bonds started strong and interest rates dipped to start the year, they reversed course in April. The benchmark 10-year Treasury note yield fell to 3.30% but steadily climbed to 4.98% in October, to levels not seen since 2007, despite inflation mostly declining along the way. The Fed maintained its higher-for-longer guidance amid four rate hikes in 2023, with potential to raise more if needed. However, while the Fed held rates steady at its November FOMC meeting, Chair Powell’s comments after were softer than its statement and bonds rallied along with the stock market. At its last meeting of the year, the Fed held rates steady again but “dovishly pivoted” to acknowledge the balance of risks now tilted to sustainably lower inflation going forward, and additional hikes were likely not only no longer needed but that rate cuts would be warranted in 2024. Inflation fell to 3.4% in 2023 from 6.5% ending 2022. Bonds rallied to year end and interest rates plunged. November and December were the 7th best two months for bonds since 1926. The benchmark Bloomberg Aggregate Bond index erased its -1.2% loss at the end of Q3 to finish UP 5.5% for the year. The benchmark 10-year T-Note yield fell 1.10% from its October peak to close unchanged on the year at 3.88%. Simply remarkable moves.

The Tale of the Tape for 2023 for investors was to maintain a long-term perspective and stay disciplined. There were many exit ramps amid many challenges and again, investors that maintained their resolve were well rewarded. Timing the market is impossible.

The Outlook

Following a very strong 2023, especially with the massive rally in stocks and bonds in November and December, could present some early challenges and consolidation of those gains. However, there is reason for optimism in 2024, albeit with some caution. Many headwinds that prevailed heading into 2023 and elevated investor and market anxiety have either subsided or are trending in the right direction.

Reason for optimism in 2024

- Recession Risk is lower with an economic soft landing the base case (mild recession still possible)

- The Fed is done raising interest rates and projections are for 3 rate cuts in 2024 (Dec-23 FOMC), while the market is expecting 6 cuts

- Financial conditions have eased meaningfully from October peak

- Inflation has decreased nearly two-thirds from its June 2022 peak and trending towards the Fed’s 2% target, though the “last mile” will be more challenging

- Corporate earnings are expected to rebound in 2024

- Diversification important for attractive long-term valuation exposure: International, Value stocks, and Small-Caps

- Presidential Election years have historically been positive, though no guarantee for future success

2024 headwinds that may present challenges and lead to volatility

- Stock valuations are elevated, especially large-cap growth stocks and the S&P 500 in general

- Volatility likely to be higher in 2024

- Economic slowdown is greater than expected

- Rekindling of inflation that may disrupt projected Fed rate cuts

- Debt ceiling negotiations and possible government shutdown

- Geo-Political Risks that may go beyond the war in Ukraine and escalating conflict in Gaza

In Summary

We are looking for continued progress on the inflation front and a soft landing for the economy in 2024. However, a soft landing does mean a slowdown from current strong levels and an uptick in unemployment, which are consistent with the Fed’s inflation objectives. A mild recession is still possible. We anticipate volatility to be higher in 2024 and will require investor patience.

The reasons for optimism above outweigh the headwinds and translate to attractive but more modest return potential for stocks. With bond yields over 4.0%, any Fed rate cuts resulting in a decline in market interest rates equates to solid bond total return potential. We emphasize investors value the importance of diversification, discipline, knowing your risk-tolerance and maintaining a long-term focus for a successful 2024 and beyond.

Call your Nelson Advisor today at 800-345-7593 to discuss any concerns and review your portfolio.

~Your Nelson Securities Team

*Past Performance is No Guarantee for Future Results