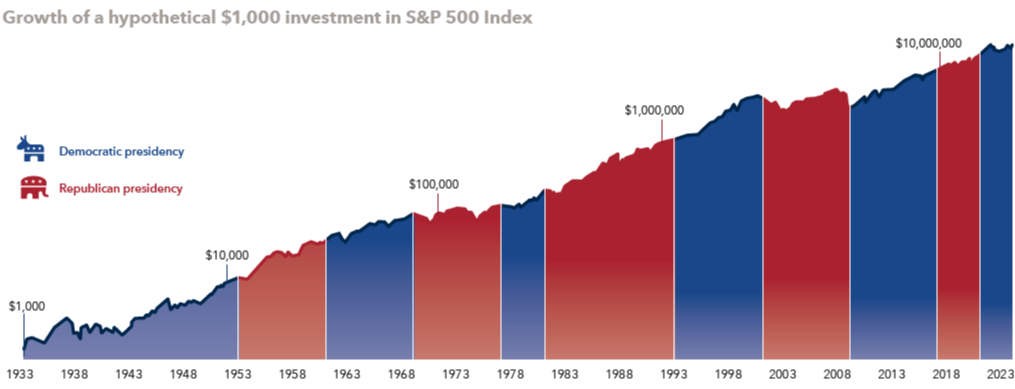

We have reached the Mid-Year point in a presidential election year. As we have noted numerous times and as our distinguished investment partners like Capital Group, Vanguard, Hartford Funds, and Dimensional Fund Advisors have illustrated, presidential election years have historically been positive. Though past performance is no guarantee for future results, the markets have followed suit ending Mid-Year 2024, and in record setting fashion no less.

Q2 saw numerous all-time highs for the tech-heavy Nasdaq and S&P 500. The benchmark S&P 500 has already set 31 all-time highs in 2024. The Dow Jones Industrials closed above 40,000 for the first time ever in May. The second quarter wasn’t without volatility; the market had a solid 4%+ pullback in April following a strong first quarter and warmer than expected inflation readings in February and March that further reduced Fed rate cut expectations causing interest rates to rise sharply.

In many ways, Q2 was a tale of two markets, with very strong gains for large-cap growth companies led by the Magnificent Seven coupled with negative returns for mid- and small-cap stocks. The same disparity can be said for growth versus value stocks and June was a microcosm of Q2 overall. The tech-heavy Nasdaq led the Q2 charge surging 8.3% and pushed its Mid-Year gain to 18.1%. The benchmark S&P 500 gained 3.9% in Q2 and closed June up 14.5% for the year. The market may have pulled forward some Second Half returns in these key areas and may not continue the blistering pace. On the other side of the market, the Dow Jones Industrials dipped 1.7% in Q2 but closed +3.8% YTD. Mid- and small-cap stocks struggled in Q2, with the S&P 400 and Russell 2000 falling 3.8% and 3.6% respectively, but still finished Mid-Year in positive territory +5.3% and +1.3% YTD.

Q2 was mixed overseas as well, with developed markets dipping 1.4%, as measured by the MSCI EAFE index, but remained up 3.5% YTD. However, the MSCI Emerging Markets index gained 4.4% in Q2 to close Mid-Year up 6.1%. The European Central Bank (ECB) cut policy rates by 0.25% in June, despite inflation remaining above its 2.0% target. This move gave the Fed cover for a similar move later this year, as well as the Bank of England (BOE).

The Bloomberg Aggregate Bond index’s 0.1% return would suggest a relatively boring second quarter. That would be far from the case as the benchmark 10-year Treasury note yield ranged from a high of 4.70% in April to a low of 4.22% in June, before ending Q2 at 4.36%. With the US economy continuing to surprise on the upside, strong job gains, and low unemployment further supporting the soft-landing narrative, warm CPI inflation numbers in February and March rattled the bond market and Fed rate cut expectations dwindled to just one or 2 by year-end. However, the bond market rallied in June with Bloomberg Aggregate Bond index gaining 1% to finish Mid-Year down just 0.7%.

The Outlook

Despite the impressive Mid-Year gains, the outlook for the second half of the year remains cautiously optimistic, with several key factors to watch:

- US Economic Growth: Continues to outpace other G7 economies with low recession risk.

- Corporate Earnings: Expected to grow double digits year-over-year for 2024 and 2025, supporting current valuations.

- Market Broadening: Anticipation of a broader distribution of market returns.

- Overseas Valuations: Remain attractive compared to US stocks.

- Bond Market: May yet post solid returns for 2024 given attractive yields.

- Inflation: Slight easing in Q2, with continued monitoring of inflation and interest rate trends.

- Job Market: Remains strong but saw a slight uptick in unemployment in May and June, though unemployment remains very low overall.

- Federal Reserve: Market expectations are for one to two rate cuts by year-end and more aligned with the Fed’s projections.

- Market Volatility: A near-term pullback would be normal after strong first half gains; volatility is expected to increase as the presidential election approaches.

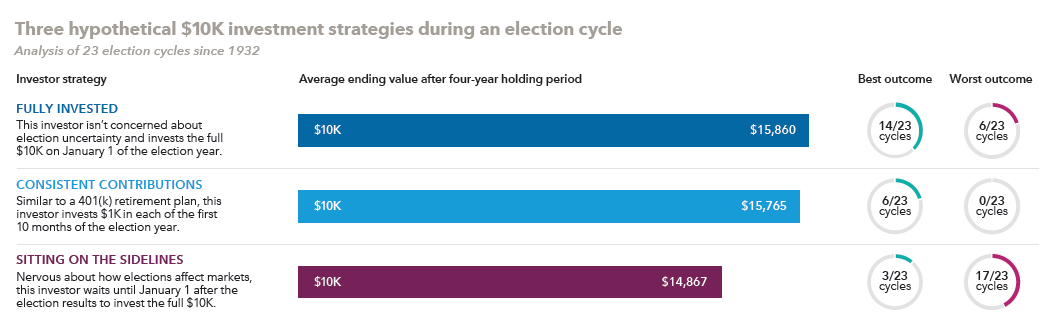

- Maintain Long-Term Focus: Look beyond the presidential elections for your investment portfolio.

Key Takeaways

- The market has shown resilience despite changes in Fed rate cut expectations and volatility.

- Large-cap growth and technology stocks have driven gains, while smaller-cap and value stocks have underperformed.

- The US economy’s strength supports the outlook, though inflation and interest rates remain key variables.

- Historical trends suggest that presidential election years are often positive for markets, though this is not guaranteed.

Conclusion: The Mid-Year performance in 2024 has been strong, at least from the large-cap perspective, which represents 70% of the total US market, and overseas markets have been solid as well. While there are risks and uncertainties ahead, particularly the November Election, the overall outlook remains positive with several supportive factors in place for the second half of the year.

During periods of uncertainty and volatility, it is important investors:

- Remain well-diversified

- Maintain discipline and patience

- Focus on the long-term

- Review your Risk Tolerance

Call your Nelson Advisor today at 800-345-7593 to discuss any concerns and review your portfolio.

~Your Nelson Securities Team

*Past Performance is No Guarantee for Future Results