Market Commentary - December 2025

Read the Fall 2025 WAA for our Market QuickTakes, Q3 Review, and Much More

December 2025

Global equities show resilience amid volatility in November

Financial markets navigated a volatile but ultimately constructive month in November as equities, bonds, and global markets reacted to shifting monetary policy expectations, political uncertainty, and strong corporate earnings.

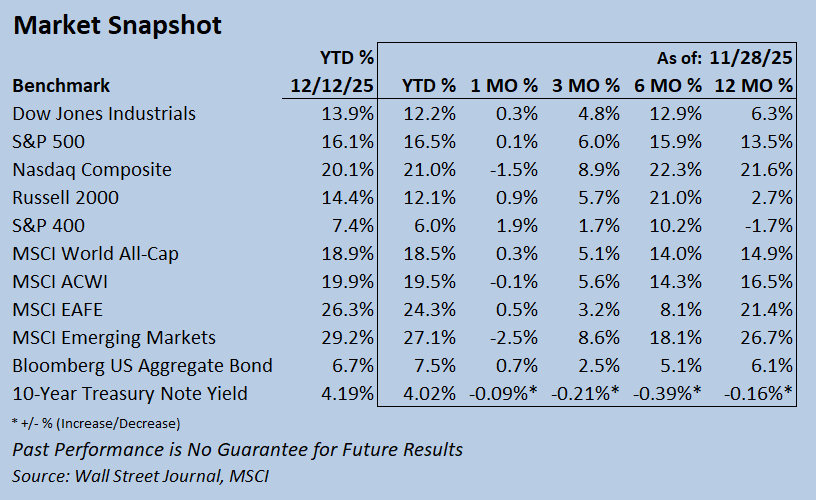

Despite a choppy mid-month pullback, U.S. stocks generally edged higher in November, supported by a late-month rally and continued resilience across sectors. Volatility surged to its highest level since April’s tariff-driven selloff as expectations for a December Fed rate cut initially collapsed. However, both volatility and rate-cut probabilities reversed course following modest inflation data released late in the month.

Small-cap and growth stocks bore the brunt of early declines, with the Russell 2000 and Nasdaq falling 8.5% and 7.9%, respectively, from their October highs. By month-end, the Russell 2000 had staged an impressive rebound to finish up 0.9%, while the Nasdaq narrowed its monthly loss to 1.5%.

Large-cap benchmarks fared somewhat better. The Dow Jones Industrial Average and S&P 500 recovered from their November lows to record modest gains of 0.3% and 0.1%, respectively. Notably, the Dow closed above 48,000 for the first time, marking a new all-time high. Mid-caps also outperformed, with the S&P 400 rising 1.9% for the month despite the temporary pullback.

The third-quarter earnings season concluded in November with broad strength across sectors. According to FactSet, 83% of S&P 500 companies reported upside earnings surprises, while 76% beat revenue expectations. These strong results continued to support market valuations and provided a fundamental anchor during a volatile month.

A significant source of policy-related uncertainty eased on November 13 when the record 43-day U.S. government shutdown came to an end. The absence of regular economic data releases during the shutdown contributed to market choppiness earlier in the month, particularly as investors attempted to gauge the underlying economic momentum without key indicators.

Global equities experienced similar volatility. After retreating from a fresh all-time high reached on November 12, the MSCI EAFE Index recovered to post a 0.5% monthly gain. Emerging Markets, by contrast, paused after strong year-to-date performance, declining 2.5% in November, yet remained the standout performer in 2025 with a 27.1% YTD gain.

Interest-rate markets swung widely in November as investors reassessed the likelihood of a December Fed cut following the central bank’s 0.25% rate reduction in late October. The Bloomberg Aggregate Bond Index fell roughly 1% from its October peak by mid-month before rallying to finish the month up 0.7% as expectations for additional easing strengthened.

Treasury yields moved modestly lower, with the 10-year Treasury Note closing November at 4.02%, down 0.09% from the previous month.

Market Update: December 2025

Following a bumpy November, expectations for another Federal Reserve rate cut in December rebounded, helping pull stocks out of their recent bout of volatility.

As widely expected, the Fed cut its policy rate by 0.25% on December 10—its third consecutive cut and the sixth since September 2024—for a cumulative reduction of 1.75%. At the same time, policymakers lowered their projected number of rate cuts for 2026 to one, down from two previously.

Despite the more cautious forward guidance, equity markets rallied on the announcement and went on to set multiple all-time highs the following day. New records were reached by the Dow Jones Industrial Average, the S&P 500, the small-cap Russell 2000, and—finally—the mid-cap S&P 400. Overseas markets also participated in the rally, with the MSCI EAFE index hitting an all-time high, alongside global benchmarks including the MSCI ACWI and the MSCI World All-Cap Index.

In fixed income markets, interest rates initially dipped following the Fed’s announcement. By week’s end, however, short-term market rates continued to move lower while intermediate- to long-term yields edged higher.

The Outlook

With year-end 2025 just weeks away, year-to-date returns for U.S. and international equities—as well as bonds—remain impressive and well above historical averages. This performance is notable given a year marked by significant challenges, including the tariff-driven selloff in early April and the record U.S. government shutdown.

For diversified, disciplined, and patient investors, the market’s recovery has been rewarding. Still, both opportunities and risks remain. Elevated valuations, ongoing economic and inflation uncertainty, and reduced expectations for future Fed rate cuts suggest that volatility is likely to persist as the balance of risks continues to shift.

As we look ahead to 2026, we believe maintaining a long-term investment process remains essential. We continue to emphasize discipline, patience, and diversification as the most reliable path forward in an evolving market environment.

Call your Nelson Advisor today at 800-345-7593 to discuss your portfolio and any concerns.

~ Your Nelson Securities Team

*Past Performance is No Guarantee for Future Results; This article is for informational purposes only and does not constitute investment advice.